In recent years, an unimaginable amount of technology and innovation has expedited the adoption of digital mortgage. Digital has ramped up borrower expectations and revolutionized traditional mortgage buying process.

Mortgage customers now expect pro-active and quick loans – as simple as purchasing their favourite book online or shopping groceries from Amazon.

Mortgage Industry’s laser focus on digital continues, however, it is essential to understand the forces accelerating this trend.

With ever-changing customer demands, gone are the days when the borrower had to fill out lengthy application forms and piles of documents. The digital mortgage application does not require much work on the part of customers; lenders can now obtain most of the information they need through third-party data providers and aggregators.

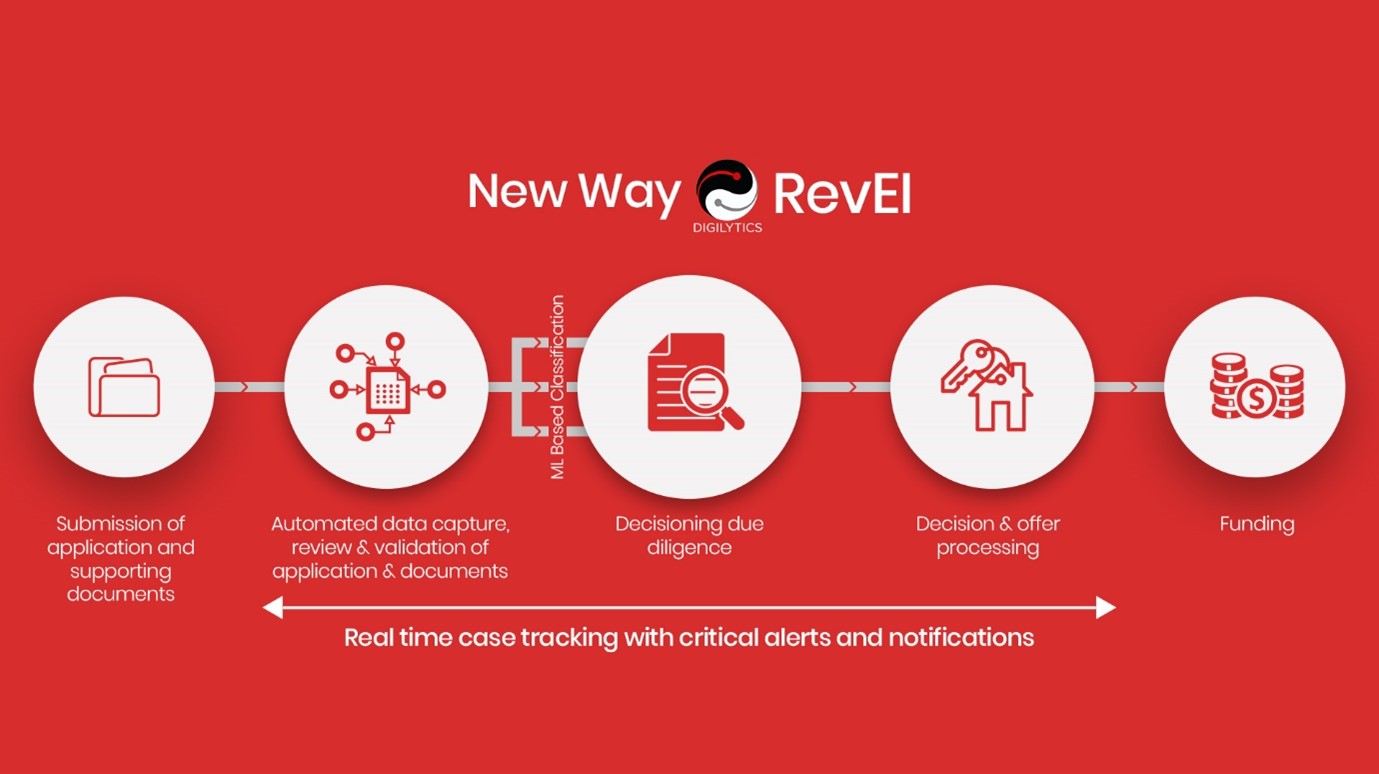

The documents are collated in different formats (pdf, images etc.) from multiple sources (portal, 3rd party providers, internal databases etc.). This helps the lenders to address the challenges introduced by fragmented and non-collated case material to get complete control, audit compliance & a single source of truth, abolish non-value-add manual data entry, add intelligence & immensely enhance the user experience.

Once we have juxtaposed sufficient data using OCR and computer vision technology, the documents are split, identified, and classified into defined file structures and categories, using text mining and machine learning algorithms.

The appropriate data is extracted from active documents using natural language processing and context learning in a format to easily verify and modify.

This assists the lenders to efficiently categorize the documents and prescribe the most beneficial loan option for the borrower demands, means and choices.

Data validation and checks are done on the documents collated, by cross-referencing across all data, i.e. from documents and external sources. Several checks are done for completeness, correctness, and consistency to generate a report at the case, document and field levels using business rules and machine learning trainable models.

This automated mechanism augments borrower experience and helps them make informed judgments, with certainty. Unlike the past, these automated approvals are based on fully verified customer financials, accuracy, and logic. There are fewer chances of going wrong, and less surprise and stress for everyone involved.

The validation report is presented to human for final approval and necessary actions on approval of data that is fed into downstream applications.

With real-time case tracking, critical alerts and notifications, the lenders can better accommodate a digital consumer, using data, advanced analytics, and artificial intelligence to eliminate steps and improve the process.

Chatbots powered by AI could suggest personalized loan products to people endeavouring financial advice, assist customers with their loan applications and take charge of service requests.

The process ends with electronic closing, which saves borrowers the difficulty of having to meet a closing agent in-person, enables them to review the closing documentation at their own time and discuss any concerns. This zeroes down the chances of delays caused by a last-minute glitch in the documentation.

The prospect of digital lending will diminish the friction associated with the financing process, eliminating paper, and moving all the tracks of the customer journey to an online and mobile capability.

Additionally, digital lenders are also using AI systems to observe borrowers’ profiles and analyse their transaction history.

Perpetual innovation is vital. Implementing a standard digital experience is not sufficient – the processes need to be agile and aligned instantly based on emerging customer expectations.

More innumerable customers today anticipate their financial services providers to offer personalized products and services which are precisely created to meet their needs, decisions, and purposes.

The lending of tomorrow will involve the comprehensive usage of an ample range of technologies including Artificial Intelligence, Analytics, Chatbots, Internet of Things, Voice-based recognition, Machine Learning, Computer Vision, Virtual Reality, Augmented Reality, Robotics Process Automation and many others.

Innovative lenders need to forecast customer needs in advance and offer a trendsetting customer experience.

Numerous lenders understand the significance of building digital mortgage capabilities into their business. However, most of those lenders also appear to be grappling for several reasons.

How long will it take the rest of the industry to catch up?

This question is worth finding an answer for!

The answer lies in decoding the fast-paced advancements taking place in the mortgage sectors, every day, every second as we speak.

While you are here, other top articles you might be interested in 1. Tech Enablers in the Mortgage Industry 2. Digilytics AI wins product of the year 2020 3. COVID-19 and the Mortgage Lenders 4. Top 5 Real Challenges in Building Predictive Models in Mortgages